Managing Your Money at 50, 60, 70

Money is so much more than just cold, hard cash. How we relate to money is often highly emotional, and our personal monetary profile is as unique as our DNA. But whatever your feelings, history and background may be, mid-life to later life require a realistic look at your present, and anticipated financial future.

We aren’t fans of long, long looks into the rear-view mirror, at least in the context of Woulda-Coulda-Shoulda, or regret. However, it is useful to orient yourself in relative terms with fairly universal financial realities. This initial grounding will help you determine what to do next. Consider this: the National Institute on Retirement Security, a non-profit research center, reports that women are 80 per cent more likely than men to be impoverished at age 65 and older. Women age 75 to 79 are three times more likely.

Let’s begin with looking back at your financial moves in your 40s. If you bought a home when you were young, and paid it off as you retired, your net worth will be equivalent to at least the value of your home. This will make affording your retirement lifestyle much easier. Combining a generous 401(k) with a paid-off house will generally assure you of a comfortable retirement. And, if you’ve owned more than one property, real estate will likely prove an excellent source of passive income.

Ideally in your 40s, you began to make the shift from capital accumulation to capital protection, with the goal being to shield yourself from illness, or just a bear market. Your 40s are the time to write a will, create a revocable living trust (better than a will, especially if you have children), invest in life insurance and set up a 529 plan – (tax-advantaged educational savings, typically established by parents and grandparents for a child who is an account beneficiary) if you haven’t already. It’s also to your advantage to free yourself from student loan debt and revolving consumer (credit card, home equity) credit, by retirement age.

Moving on from your 40s, where are you today? For most retirees, shelter and healthcare costs are the two main expenses. Here are some quick, retirement-age benchmarks to assess your financial health throughout your 50s, 60s, 70s and beyond.

Your 50‘s

It’s time for some strong coffee and a freshly sharpened pencil as you take a hard look at retirement income planning.

1- This begins with a side-by-side analysis of three crucial factors:

INCOME

SAVINGS

EXPENSES

2- Review your investment allocation

3- Explore additional retirement income sources, including a deferred income annuity

4- Now for a hard conversation: start planning for long-term care, in the form of long-term care insurance and funding strategies. These are best purchased and reviewed in your 50s. Once you get into your 60s, it may be harder to qualify for coverage.

5- Looking forward, get serious about family and next-generation planning.

6- Aggressively beef up your taxable investments. These assets will give you the confidence to retire gracefully in your 60s. The goal is to accumulate a taxable investment portfolio that is 2X to 3X larger than your pre-tax investment accounts such as your 401(k) and IRA, so utilize as much of your free cash flow as possible to build your taxable investment portfolio.

Here’s an after-tax investment account guide to consider:

The bottom line for your 50s:

A good rule of thumb is to have saved 25X what you plan to spend each year in retirement, or 8X to 15X your current salary. Your 50s are the time to decide how long you’ll work, and thus what your Social Security benefits will be, which are key factors in how much you need to save in order to comfortably retire.

Your 60’s

In your 60s, the gloves come off. Financial planners may ask you point-blank how long you think you’ll live! It’s a fair question from the standpoint of crunching the numbers, but it’s a metric no one ccan accurately produce. Boomers typically are living longer than their parents, for instance.

- Longevity is a blessing, and it can be an expensive blessing in the form of health care, long-term care, and inflation, all of which threaten the sustainability of your retirement income.

- So, now’s the time to get real. Plan out how you’ll generate income, when you plan to retire if you have not done so already, and when you’ll file for your Social Security.

- Remember that Social Security was never intended as the sole source of income for retired people. Unfortunately, for many millions of Americans who lack the legacy of inherited generational wealth, SSI is a literal lifeline. The likelihood is that this underfunded national pension system will continue to exist, but it’s not enough to afford a comfortable retirement on its own. Check out this quick calculator to estimate your benefits: https://www.ssa.gov/oact/quickcalc/

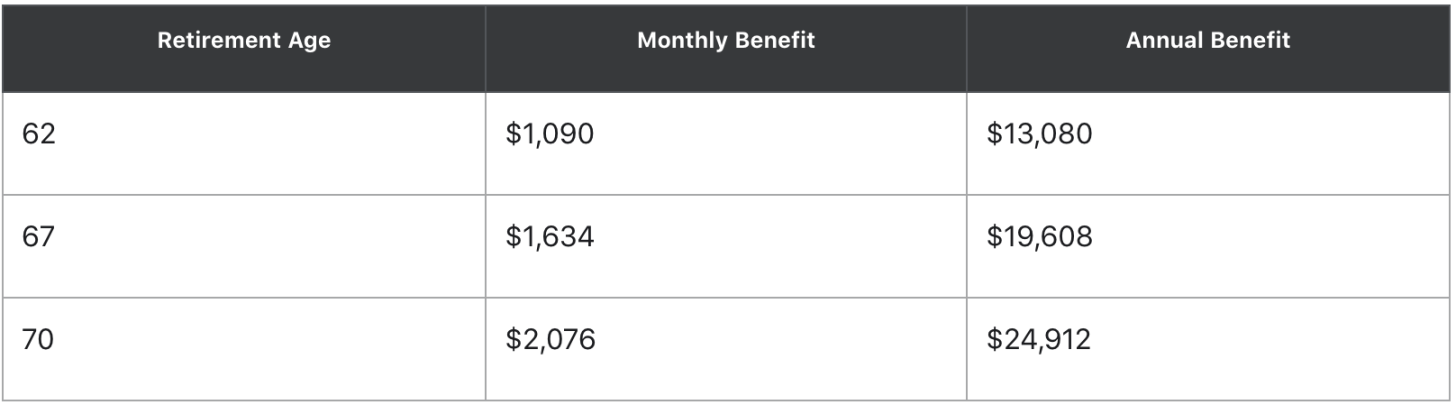

Expert opinions vary about when to file. And individual circumstances do factor into the decision. If you’re in good health, hang in there until 70 (unless your advisor gives you a good reason to do otherwise). If your health is an issue, do what you have to do. However, it’s a fact that if you wait until you turn 70 to collect, your Social Security benefit will be almost double.

The bottom line for your 60s:

Ideally, you have saved 10X to 25X your current salary, depending on spending goals and other income sources. Financial experts state that ideally, your net worth should now be at least 25X your annual expenses, or 20X your average annual gross income. Reaching these benchmarks is your key to financial freedom.

As you head into retirement, make sure you understand the 4% safe withdrawal rate for retirement spending. The rule states that historically in the U.S., with a 50% bond investment and a 50% stock investment, you could afford to spend 4% of your investments a year and not run out of money for 30 years. This is a conservative approach, but it does give a good starting point on how much you can spend in retirement.

Your 70’s

This is a time of reckoning. The question of income is simpler now than it was a few decades ago. You may have passive income vehicles, a very good thing indeed. You probably have filed for Social Security, also a good thing. And most likely, although the exception proves the rule, you are no longer working full-time for a salary.

Here’s a cautionary tale: many people rely on friends and family members to guide their financial decisions. Our advice: just don’t. Instead, hire a professional financial advisor and broker. Angst and confusion may cause us to back off from the entire process, but doing this puts you at a tremendous disadvantage. Educate yourself. Start with a look at a Retirement Planning Calculator. It’s no substitute for sitting down with a skilled professional who can break down all of the elements — your assets, your risks, and more — and help you navigate the landscape of income events, spending goals and other variables.

- Now, this will sound morbid. But one of the greatest advantages of working with a professional financial planner is that you can avoid dying with too much money, or rather departing this realm without an appropriate plan for the distribution of your assets (i.e., education funds for grandchildren).

- Don’t forget to plan and manage your Required Minimum Distributions (RMDs) from IRAs and 401(k)s. Optimizing these assets can require new types of planning and tax strategies.

- Enjoy, and spend. If your withdrawal rate from your assets starts approaching 8-10%, you may need to pull in the reins. Financial planners like to see a withdrawal rate of around 4% but talk about this with your expert. Obviously, sometimes fate intervenes, and we need to spend more than we originally anticipated. A sudden change in housing status, for example, may put an unanticipated drain on your assets.

- Celebrate by giving back. After you reach age 70 ½, you’ll need to take RMDs from an IRA, consider qualified charitable distributions (QCDs) that are now available to you. A QCD allows you to take a distribution from an IRA and send it directly to a charity of your choice. Doing this helps offset your RMD requirements for the year, and is not treated as taxable income. Cheers!

The bottom line for your 70s:

It’s never too late to make good financial decisions that will make your present living arrangement more comfortable and secure, and may also create a legacy for loved ones and the community and culture at large. The most important caveat is this: make your decisions upon solid data regarding your own specific financial picture, versus on something you heard from somebody else. Do not base your decisions on someone else’s apparent situation, since it’s unlikely that you know every nuance of their finances. Someone driving a new Mercedes isn’t necessarily, absolutely “doing better” than you are. Appearances may be deceiving, so don’t come to conclusions based upon how someone else lives or spends.

#

Be the first to comment