It is never too late — and never too early — to build a financial future that reflects your worth.

There’s an old saying: ‘The best time to plant a tree was twenty years ago. The second best time is now.’ If you’re a Black woman in your 50s who hasn’t yet figured out retirement savings, or who feels overwhelmed by the financial landscape, this article is written with deep respect for where you’ve been — and tremendous excitement for where you are going.

Black women face a distinctive set of financial realities: a persistent wealth gap, longer life expectancy than any other demographic group, decades often spent as primary caregivers, and a history of wage disparities that compound over time. Understanding these realities isn’t cause for despair — it’s cause for strategic, intentional action.

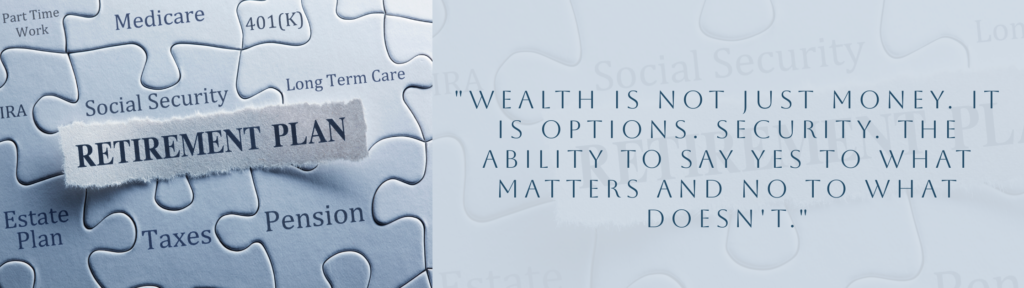

Start With a Clear Picture

Before you can build wealth, you need to know exactly where you stand. Pull together your current savings, any retirement accounts, your Social Security projected benefits (available at ssa.gov), any pension benefits, and a realistic picture of your monthly expenses — now and in the future. This moment of clarity, though potentially uncomfortable, is the foundation of everything.

Maximize Your Accounts — Especially Now

Here is powerful news for women over 50: the IRS allows you to contribute more to retirement accounts than younger workers. These are called catch-up contributions, and they are a direct gift to those of us who are building momentum in the second half.

✦ 401(k): You can contribute up to $30,500 per year (compared to $23,000 for those under 50).

✦ IRA (Traditional or Roth): You can contribute up to $8,000 per year.

✦ If you’re self-employed, a SEP-IRA allows contributions up to 25% of your net income.

Traditional vs. Roth: Know the Difference

A Traditional IRA or 401(k) allows pre-tax contributions — you pay taxes when you withdraw in retirement. A Roth IRA uses after-tax dollars — but your withdrawals in retirement are completely tax-free. For many Black women who expect to be in a similar or higher tax bracket in retirement, a Roth can be extraordinarily advantageous. Consult with a fee-only financial advisor to determine the right mix for your situation.

Social Security: Maximize Your Benefit

Social Security is often the cornerstone of Black women’s retirement income. When you claim matters enormously. Claiming at 62 reduces your benefit by up to 30%. Waiting until your Full Retirement Age (66–67, depending on birth year) gives you your full benefit. Delaying until 70 increases your benefit by 8% per year. For women with longer life expectancies, waiting as long as financially possible can mean tens of thousands of dollars more over your lifetime.

Consider a Financial Advisor Who Understands Your Journey

Not all financial advice is created equal. Seek out Black women financial advisors or advisors with deep experience working with Black women clients. Look for fee-only advisors (who charge a flat fee or hourly rate, not commissions). Organizations like the Association of African American Financial Advisors (AAAA) can be excellent resources.

It Is Never Too Late to Begin

Whether you are starting from zero at 55 or looking to optimize at 62, there are meaningful moves you can make. Reduce high-interest debt aggressively. Downsize thoughtfully if it serves your financial future. Consider part-time work you love that adds to your savings. Build an emergency fund of 3–6 months of expenses so retirement savings are never touched early.

Your financial future is being written right now. Every intentional dollar is a love letter to your future self.

Be the first to comment